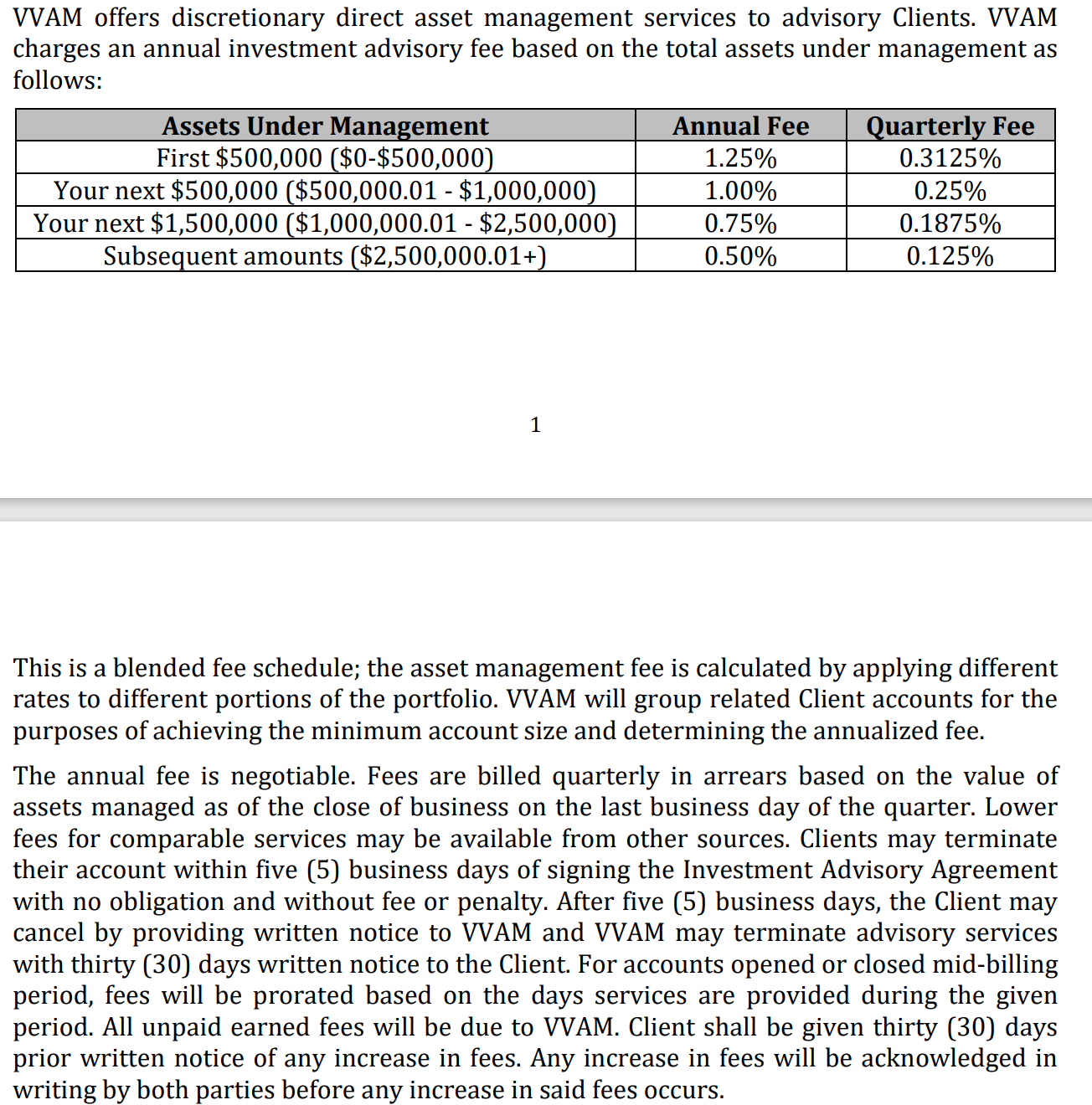

Owners of lower middle market (“LMM”) businesses contemplating a sale or majority recapitalization should be aware of trends in rollover equity in M&A transactions. As a seller of a LMM business, you may be expecting to have a full exit from your business at the closing table. Sellers may be surprised when their investment banker broaches the topic of rolling equity in a transaction and the terms of Indications of Interest (“IOIs”) and then Letters of Intent (“LOI”) include references to rollover equity in the proposed capital structure of a transaction. What is rollover equity, why is it used, and why can’t sellers always have a clean economic break from their business?

What Is Rollover Equity?

Within an acquisition, rollover equity refers to the portion of the sale proceeds reinvested by the seller(s) or ownership group of a company into the equity of the post-acquisition company, typically referred to as “Newco”. Newco is the new or acquiring entity formed by the buyer to facilitate the acquisition. The biggest reason to use rollover equity in an acquisition is to align interests through shared economic ownership. Rollover equity gives the seller(s) a “second bite at the apple”, and rollover equity is also tax-deferred if structured properly. From the perspective of a business owner, rollover equity is among the most important economic aspects of any deal and is often a focal point of deal negotiations since rollover equity reduces the sale proceeds at closing and economically ties the seller to the business for an extended period of time.

Why is Rollover Equity Used

While the overall driver to use rollover equity in an acquisition is to align interests through shared economic ownership, other factors can play a role. Creating skin in the game for sellers who may be viewed as critical to the continued operations or reputation of a business can be important to buyers. Continuity of key customer and supplier relationships may be aided by the sellers’ continued ownership interest in the business. Certain buyers may also be looking for rollover equity as a source of capital to help fund the deal and close gaps in the proposed capital structure given issues with equity capital capacity or limitations on borrowing capacity. Private equity buyers may have internal fund policies requiring rollover equity in deals.

In some deals, sellers may have sufficient conviction in the prospects of their business to insist on rollover equity to preserve exposure to the upside of the future success of the business. In our experience, a seller’s willingness to include rollover equity signals confidence in the business. After all, buyers always face some aspect of asymmetric information- a seller will always know more about their business than the buyer. Rollover equity serves as a practical mitigant to this issue and a refusal to consider rollover equity can be seen as a red flag by buyers.

Overall, rollover equity is common for acquisitions in the LMM. While no single authority on deal structure related data exists, we have seen previous surveys from M&A transaction service providers suggest that nearly 80 percent of surveyed middle market M&A transactions include some form of rollover equity and the typical amount of equity rolled in a middle market transaction is approximately 20 percent. Our view is that those figures are likely similar for LMM acquisitions. Some strategic buyers may not have a desire to use rollover equity, while acquisitions of smaller companies that serve as add-ons to larger platforms may not request rollover equity to avoid diluting the platform owners, particularly if the platform owner is close to exiting.

Potential Benefits for Sellers

A seller’s openness to rollover equity shows commitment and confidence in the business for a buyer. Retaining some ownership in the business through rollover equity provides sellers with a second bite at the apple. There are many examples of sellers receiving considerable future economic benefits from rollover equity and the most successful deals can even result in sellers ultimately receiving more proceeds from the rollover equity than from the initial transaction. Some sellers may have the opportunity to continue their ownership through multiple exits and multiple owners, getting additional subsequent payoffs stemming from the original rollover equity.

When to be Cautious with Rollover Equity

Despite the upside opportunities, there are some good reasons to be skeptical around rolling equity. If a seller has justifiable doubts around the future of the business or the industry, reducing your economic exposure to the business is prudent. Of course, bona fide concerns around the business makes the negotiating process challenging as informed buyers likely harbor similar doubts.

Rollover equity creates the need for the seller to evaluate the other side of the table. If a seller doubts the buyer’s ability to execute on the value creation thesis or successfully operate the business, rollover equity poses some challenges. One area a seller should pay particular attention to is the prudence of the proposed capital structure of the post-close company. Too much leverage in the form of senior and junior debt increases the financial risk of the deal and may impact the ability of the company to comfortably service the debt load through all operating scenarios, including downside scenarios.

Sellers also need to pay attention to mezzanine capital as most rollover equity is common stock or similar LLC units. Rollover equity is almost always at the bottom of the capital stack. Relatedly, sellers should carefully review whether rollover equity is pari passu with the buyer’s equity. If the buyers are getting preferred, sellers should focus on receiving preferred as well. If a seller is encountering a proposal to receive equity that is junior to the buyer’s equity or the buyer’s equity has some type of structural preference to the rollover equity, proceed with caution, particularly in highly leveraged deals. For situations when your business is being acquired by an existing platform and you are being offered rollover equity in the platform, pay close attention to the relative or implied valuation of the platform. A buyer may be using richly valued or overvalued platform equity as cheap currency to pursue accretive add-on deals, leaving sellers holding the rollover equity at an unattractive or speculative valuation.

Our View

In the current environment, sellers should expect some form of rollover equity. Approaching the concept openly of staying economically tied to the business after closing is helpful and will help level-set expectations at the negotiating table. However, sellers should know the drivers behind a buyer’s request for rollover equity and understand that alignment of interests is only a high-level concept. A buyer can have a variety of motivations to propose rollover equity. Situations exist where buyers seek to use rollover equity to establish a more attractive deal structure, leaving sellers junior to the buyer’s equity in a highly leveraged capital structure, with sellers in first loss position in a downside scenario. Understanding the specific terms of rollover equity is critical. Sellers should have access to advice and information to help determine if proposed rollover equity terms are within the range of “market”. In a truly aligned scenario involving the sale a quality business, rollover equity can be a significant economic benefit to sellers, who go along for the value creation ride with the new buyers and receive an attractive future payoff from the second (or third) bite at the apple.

Vail Valley Asset Management – Full Service Investment Management for Business Owners

We offer a highly differentiated investment solution for lower middle market business owners centered around our unwavering commitment as fully aligned fiduciaries. We view our clients’ business ownership as their most important asset that is at the core of our portfolio management process. At Vail Valley Asset Management, we are 100% fiduciary 100% of the time, and offer a source of objective advice to business owners. Building and operating a business is complex, requiring dedication, vision, and perseverance. Selling your company attracts sell-side service providers motivated by success fees and other deal-related fees. You deserve a trusted and unbiased advocate with a deep understanding of private markets to guide you through the complexities of the M&A process. If you are a business owner looking for a financial advisor with expertise in private markets and the M&A process, contact us at Vail Valley Asset Management to schedule a consultation.

Read Next

Vail Valley Asset Management, LLC is a Registered Investment Advisory firm located and registered in Colorado. * The firm’s services are not available in all states and the firm may need to seek additional registrations before working with a client in a state in which it is not presently registered.